27 May 2026

Volume Patterns Reveal Seasonal Edges in Global Soccer Markets

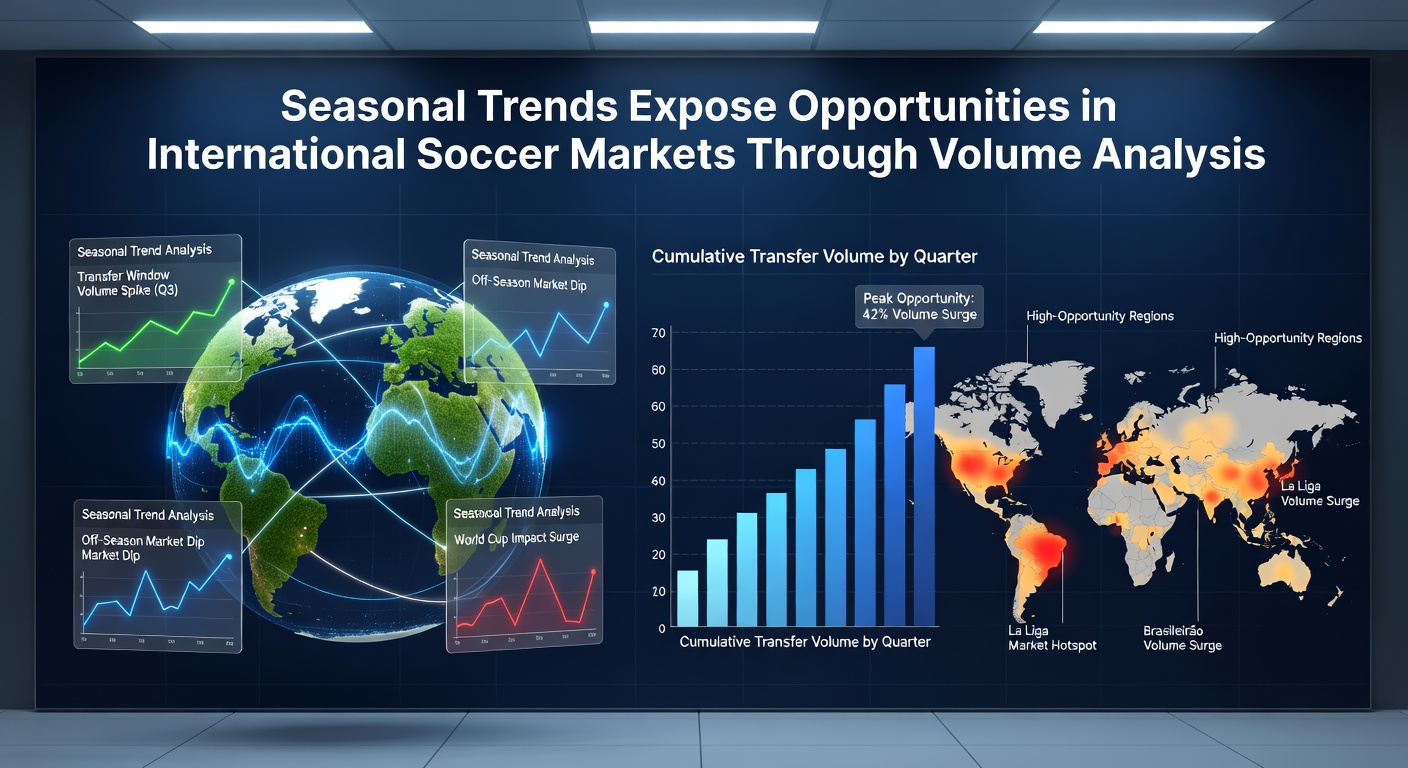

International soccer markets display distinct volume fluctuations tied to league calendars, cup schedules, and player availability windows, and analysts track these shifts through detailed order flow and liquidity metrics. Data from major European and South American competitions shows that trading activity often surges during winter breaks in northern leagues while tapering in summer months when transfer windows dominate attention. Observers note that such patterns create measurable discrepancies between expected and actual market depth, particularly around key fixtures in May when title races conclude and relegation battles intensify.

Calendar Cycles Drive Liquidity Changes

European domestic seasons typically wrap up by late May, and volume analysis from multiple platforms indicates that bettors pile into final-day matches with higher stakes than mid-season contests. In contrast, South American leagues often peak during their own summer schedules, producing cross-hemisphere arbitrage opportunities when European volume dips. Researchers at sports analytics firms have mapped these rhythms over several years, revealing consistent spikes in live betting turnover during evening kickoffs across time zones.

Volume metrics also shift around international breaks, where club competitions pause and national team windows attract separate liquidity pools. Those who monitor aggregated data across Asian and European exchanges report thinner books on club matches immediately following such interruptions, because roster uncertainty reduces sharp money participation. This thinning effect appears most pronounced in May 2026, when several European leagues face compressed schedules due to expanded continental tournaments.

Regional Variations in Market Depth

Asian handicap markets on Japanese and Korean leagues exhibit different seasonal signatures compared with Premier League or La Liga equivalents. Data indicates heavier volume concentration in the latter half of Asian seasons, coinciding with playoff qualification races, whereas European markets see steadier but lower per-match liquidity during holiday periods. Analysts compare these patterns by normalizing trading volume against fixture difficulty ratings, exposing edges where public money overweights certain outcomes without corresponding sharp participation.

One study of multi-year order book snapshots found that Brazilian Serie A totals markets widen noticeably during their winter months, creating situations where line movement lags behind actual volume influx. Similar observations hold for Major League Soccer in North America, where summer humidity and travel schedules correlate with distinct over-under volume clusters. Observers track these regional differences through timestamped liquidity heatmaps rather than final scores alone.

Practical Applications of Volume Tracking

Traders who integrate volume-weighted average price data with seasonal baselines can identify when early lines fail to reflect true market interest. For instance, midweek cup ties in February often attract less institutional flow than weekend league fixtures, allowing sharper operators to exploit slower line adjustments. Figures from independent research groups show that such mismatches occur more frequently during shoulder months when multiple competitions overlap.

Automated scraping of exchange depth charts combined with historical fixture calendars provides a framework for forecasting liquidity droughts. Those applying this method across leagues report improved timing on both pre-match and in-play positions, especially when volume thresholds deviate from five-year averages. Australian regulatory filings on sports wagering confirm that international soccer accounts for growing shares of total handle, underscoring the value of cross-market volume comparisons.

Technology and Data Integration

Modern platforms now publish granular volume feeds that allow comparison of matched amounts across bookmakers and exchanges in real time. Academic papers from European sports management programs have begun incorporating these feeds into regression models that isolate seasonal effects from team form variables. The resulting outputs highlight windows, such as post-Christmas fixture congestion, where volume surges fail to tighten spreads proportionally.

Industry reports from the European Gaming and Betting Association note steady growth in soccer-related turnover, yet seasonal granularity remains underutilized by many participants. Mapping these cycles against broadcast schedules further refines predictions, because televised matches draw retail volume that sometimes masks underlying sharp flows. Analysts therefore layer television ratings atop raw volume statistics to separate noise from signal.

Conclusion

Seasonal volume analysis supplies a quantitative lens for navigating international soccer markets without relying on outcome prediction alone. By aligning liquidity data with calendar events, market participants gain visibility into periods when edges emerge from structural rather than informational advantages. Continued refinement of these models, supported by expanding data availability, positions volume tracking as a core component of systematic approaches across global soccer betting environments.